The End of the Billable Hour

Why Legal Services Is Entering a 36-Month Restructuring Window

Argentis Labs Research · · 8 min read · Download PDF

The End of the Billable Hour: Why Legal Services Is Entering a 36-Month Restructuring Window

By the Argentis Labs Research Team

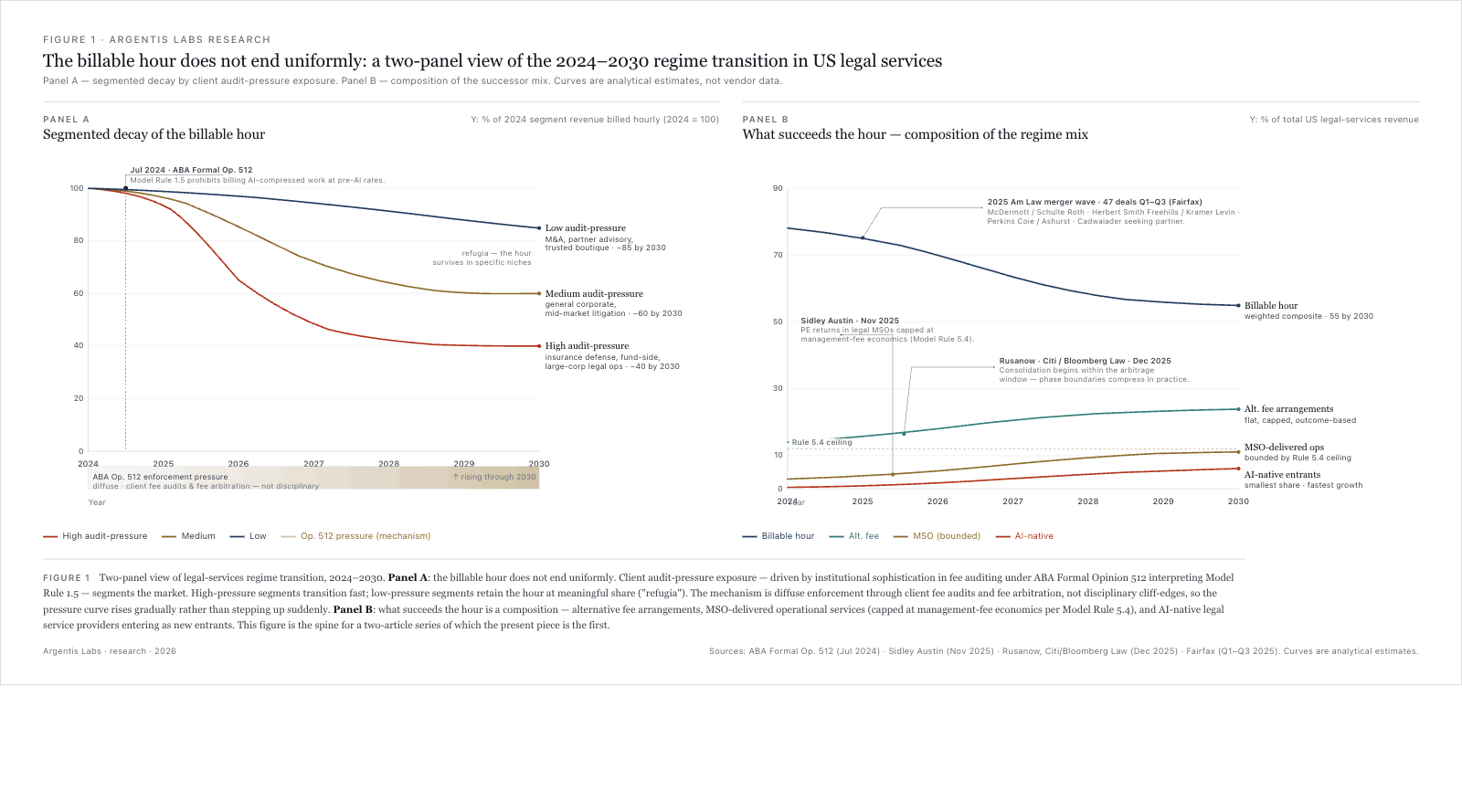

Bloomberg Law reported on December 15, 2025 that Fairfax Associates counted 47 US law firm mergers in the first three quarters of 2025, up from 43 in the same period of 2024. The named combinations are top-of-market: McDermott Will & Emery combined with Schulte Roth & Zabel; Herbert Smith Freehills with Kramer Levin; Perkins Coie and Ashurst announced a tie-up; Cadwalader Wickersham & Taft is reported to be seeking a partner. Gretta Rusanow, who runs the Citi Law Firm Group advisory practice, told Bloomberg Law in the same article that "the way to outperform your peers is to buy that growth." The question worth asking is what is driving that growth, and whether the underlying catalyst is visible elsewhere in industry data.

The 2026 Citi Hildebrandt Client Advisory, published December 11, 2025, decomposes 11.3% US law firm revenue growth through the first three quarters of 2025 into three factors: the collection of high inventory levels entering the year, 1.9% demand growth, and a 9.6% increase in rates. Only the second reflects genuine new legal work being commissioned; the first and third are firm-side propping moves.

On the other side of the income statement the composition tells its own story. Operating expenses grew 8.4% and compensation expenses grew 9.8% — the compensation line, which is where headcount investment flows, outpaced overall operating-cost growth. Total lawyer headcount grew 2.9%, but equity partner headcount declined 0.5%: every one of the added lawyers was salaried, and the income-partner tier grew 6%. On the net, the firms in these numbers are not adding equity partners. They are expanding salaried and income-partner headcount — the billable-capacity tiers — while shrinking the ownership tier, with leverage ratios rising 4.3% on the resulting mix. Citi attributes to this composition a productivity decline of 0.6%: added lawyer capacity outpacing what demand can absorb. Firms have been restructuring their partnership economics.

The resulting picture doesn't look great: revenue appears healthy only because firms pushed up rates on soft demand while burning down inventory that had accumulated entering the year. Such rate and demand growth dynamics suggest the priced product is showing stress while the pricing-regime response has not yet been structurally adjusted. As the Citi report states, 2026 is expected to bring "broader market consolidation," with the most profitable firms capturing a greater share of the market.

The share of firms recording year-over-year demand growth by segment: 69.2% of Am Law 50 firms, 51.4% of Am Law 51–100 firms, 64.4% of Am Law Second Hundred firms, and 61.5% of firms outside the Am Law 200. Market concentration of this shape typically precedes visible merger activity by one to two reporting cycles, because the losing segment first absorbs the pressure through margin compression and leverage adjustments before it surfaces in an announced combination. The 47 Q1–Q3 mergers above are the tail-end expression of this divergence.

Taken in aggregate, the merger data, Rusanow's "buy that growth" framing, and the revenue-composition breakdown describe a market in which rate and inventory are doing the work that organic demand is not. Such conditions resolve through consolidation rather than demand rebound.

The "rule layer" moved at nearly the same time, compounding rather than relieving the pressure. On July 29, 2024, the ABA Standing Committee on Ethics and Professional Responsibility issued Formal Opinion 512. Trade coverage has emphasized the supervisory reading — that the attorney using generative AI retains duties of competence, confidentiality, communication, and supervision. The Opinion itself is load-bearing since it closes three workarounds through which firms might otherwise preserve the billable-hour revenue model against the efficiency AI tooling delivers.

A lawyer on hourly billing cannot charge for hours not actually expended, however efficient the lawyer has become; the opinion reads Rule 1.5 to foreclose billing "more hours than were actually expended on the matter." The flat-fee escape hatch is closed next: a fee quoted at pre-AI rates and delivered with AI-assisted tooling is described in the opinion as potentially "a fee charged for which little or no work was performed," which it treats as unreasonable per se. And the cost of becoming AI-literate cannot be passed back to clients — the opinion locates AI fluency inside the underlying duty of competence, a precondition for practicing under the rule rather than a billable line item amortizable across a book of matters.

The combined effect is that Opinion 512 does not only codify human oversight. It closes the escape hatches — phantom hours, legacy flat fees, learning-curve passthrough — through which the efficiency would otherwise be routed back into a preserved hourly revenue stream. Thus, firms must instead restructure the pricing model away from the hour toward something AI-assisted delivery can inhabit without violating Rule 1.5 — fixed-fee engagements with productivity terms, outcome-based pricing, subscription arrangements, or management-services structures that isolate legal fees from the operating margin. The accounting vertical has already traveled this road under professional-responsibility constraints of its own and produced a specific structural answer, which the next section takes up.

Three PE-backed transactions in the last 24 months reshaped the top of the US accounting market through what the profession calls the Alternative Practice Structure, or APS: the firm bifurcates into a licensed CPA entity that retains attest and audit practice and remains accountant-owned, and an advisory entity that can take outside investment. New Mountain Capital took a majority stake in Grant Thornton, then the seventh-largest US accounting firm by revenue, in a transaction that closed on May 31, 2024, and was reported by Accounting Today as the largest PE investment in the profession to date. Blackstone acquired a majority stake in Citrin Cooperman from New Mountain at a $2 billion valuation announced on January 7, 2025 — Inside Public Accounting called the transaction the sector's first PE-to-PE flip of an audit firm. Apax Funds acquired a majority stake in top-20 firm CohnReznick, announced in February 2025 and closed by the end of April (Journal of Accountancy, February 2025).

What the accounting APS wave establishes is that the regulatory form for sequestering outside capital from the "professional responsibility constrained" practice is both shippable and financeable at scale. The firms that executed it restructured ahead of a regulatory environment that had not forced them to — rate pressure, succession obligations to retiring partners, and competitive capital needs were the operative drivers, not bar-council enforcement. Legal is at the same moment under sharper constraint. The accounting firms moved ahead of regulatory forcing; legal is moving under it — Rule 1.5 already foreclosing the hourly-revenue workarounds, and the market-share data above already recording consolidation in progress.

APS' analogue in legal services is the Management Services Organization (MSO). Sidley Austin's November 25, 2025 analysis of private-equity investment in US law firms describes what separates the MSO from accounting APS in a specific, binding way. The MSO structure splits a law firm into two entities: the legal practice entity, which handles legal representation and may receive legal fees, and the management-services entity, which handles back-office operations — billing, technology, human resources, marketing, real estate — and is paid a management fee by the legal practice entity through a master services agreement. Under Model Rule 5.4, only the legal practice entity may receive legal fees. PE returns in a legal MSO are accordingly capped at management-fee economics: outside capital cannot participate in the revenue-generating legal-fee line itself. This contrasts with accounting APS, in which the advisory entity — the outside-investment vehicle — is itself revenue-generating. The Texas Commission on Professional Ethics has ruled that lawyers and outside investors may hold equity in an MSO, but that the MSO may not be paid a portion of legal-fee revenues, and must not engage in unauthorized practice of law. The legal MSO is a constrained form of the accounting APS. The constraint shapes what PE-backed legal consolidation will look like without invalidating the thesis that it will occur.

Three structural conditions now hold simultaneously: expenses outpacing demand, productivity turning negative, revenue carried by rate and inventory rather than by new work. Model Rule 1.5 forecloses capturing the compression AI tooling creates inside the billable hour, closing the most obvious short-run pricing responses. And the accounting vertical has demonstrated that the APS form for admitting outside capital to a professional-services restructure is both executable and financeable at scale, with the legal MSO as a constrained adaptation. The window for firms to restructure on their own terms is roughly 36 months wide before regulatory-enforcement norms, insurer panel-counsel programs, and corporate outside-counsel rate cards converge on AI-assisted delivery as the baseline. The clock is running. What capital flows into legal consolidation, at what multiples, and through which MSO-adapted structures the constraint permits, is the question the next piece in this series examines.

<!-- word count: 1583 -->